Estimasi Parameter Model Autoregressive dengan Metode Yule Walker, Least Square, dan Maximum Likelihood (Studi Kasus Data ROA BPRS di Indonesia)

Article Sidebar

Main Article Content

Abstract

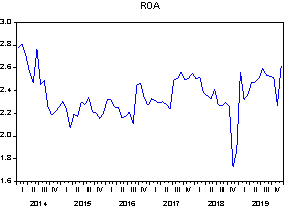

The Autoregressive model is a time series univariate model for stationary models. In estimating parameters on this model can be done by several methods, namely yule-walker method, Least Square, and Maximum Likelihood. Each method has a different principle for estimating model parameters so that the results obtained will also be different. Based on this, in this study, the AR(1) model parameter estimation was estimated by generating data simulated 1000 times to see the performance of Yule-Walker, Least Square, and Maximum Likelihood methods. In addition, the comparison of these three methods is also done on ROA BPRS data that follows the AR(1) model. The results showed that the Maximum Likelihood method was able to provide mode results and comparison of the most suitable estimation results for simulation data and produce the smallest MAE values in the data in sample and MAPE, MSE, and MAE the smallest in the out sample data. These results show that the Maximum Likelihood method is the best method for modeling data that follows the AR(1) model.

Article Details

Section

How to Cite

References

N. Wirawan, Cara Mudah Memahami Statistika Ekonomi dan Bisnis (Statistika Deskriptif), Denpasar: Keraras Emas, 2012.

D. Rosadi, Analisis Runtun Waktu dan Aplikasinya dengan R, Yogyakarta: Gajah Mada University Press, 2016.

W. W. S. Wei, Time Series Analysis: Univariate and Multivariate Methods Second Edition, Boston, MA, USA: Pearson Education, 2006.

A. Widarjono, Ekonometrika Pengantar dan Aplikasinya Disertai Panduan EViews, 4 ed, Yogyakarta: UPP STIM YKPN, 2017.

D. Rosadi, Ekonometrika & Analisis Runtun Waktu Terapan dengan EViews, Yogyakarta: Andi Offset, 2012.

B. Prabawa, J. Nasri, dan M. D. Sulistiyo, “Prediksi harga saham dengan menggunakan metode autoregressive dan algoritma kelelawar,” e-Proceeding Eng., vol. 2, no. 1, pp. 1696–1704, 2015.

Y. H. Mahendra, H. Tjandrasa, dan C. Fatichah, “Klasifikasi data Eeg untuk mendeteksi keadaan tidur dan bangun menggunakan autoregressive model dan support vector machine,” JUTI J. Ilm. Teknol. Inf., vol. 15, no. 1, pp. 35-42, 2017, doi: 10.12962/j24068535.v15i1.a633.

E. D. Feigelson, G. Jogesh Babu, dan G. A. Caceres, “Autoregressive times series methods for time domain astronomy,” Front. Phys., vol. 6:80, Aug. 2018, doi: 10.3389/fphy.2018.00080.

V. Gupta dan M. Mittal, “KNN and PCA classifier with Autoregressive modelling during different ECG signal interpretation,” Procedia Comput. Sci., vol. 125, pp. 18–24, 2018, doi: 10.1016/j.procs.2017.12.005.

B. Jin, J. Guo, D. He, dan W. Guo, “Adaptive Kalman filtering based on optimal autoregressive predictive model,” GPS Solut., vol. 21, no. 2, pp. 307–317, 2017, doi: 10.1007/s10291-016-0561-x.

Hery, Analisis Kinerja Manajemen, Jakarta: Grasindo, 2014.

A. Sugiono dan E. Untung, Panduan Praktis Dasar Analisis Laporan Keuangan, Jakarta: Grasindo, 2016.